-

Call: +91-9840269190

Call: +91-9840269190

-

Mail: hr@voltechgroup.com

Mail: hr@voltechgroup.com

How to Ensure Compliance with Indian Labor Laws When Outsourcing Payroll

How to Ensure Compliance with Indian Labor Laws When Outsourcing Payroll

- By Muthamizh.P

- Published: 31 May 2026

- Written by Muthamizh.P , I've been working in HR operations, payroll administration and statutory compliance for over 5 years. Through my work, I regularly interact with HR leaders, payroll professionals, compliance experts and business owners to understand the real-world challenges organizations face in managing payroll and labor law compliance across India. The insights shared in this article are based on those conversations, industry developments and practical experience with payroll processes, compliance requirements and workforce management. My goal is to help employers and HR professionals better understand complex compliance topics and make informed decisions when managing or outsourcing payroll.

Key Takeaways:

Outsourcing payroll delivers measurable benefits for large-scale and mid-scale Indian companies: lower cost, specialist statutory expertise and reduced administrative load. However, outsourcing payroll execution does not transfer the employer's statutory obligations under Indian law. The Employees Provident Fund Organisation (EPFO), Employees State Insurance Corporation (ESIC) and Income Tax Department issue penalties, interest demands, and prosecution notices directly to the registered employer - not to the payroll processing vendor.

This guide is designed for HR managers, business owners and compliance officers at organizations with 50 to 5,000+ employees who need to outsource payroll while maintaining full legal defensibility.

What Indian Labor Laws apply when you Outsource Payroll?

Payroll outsourcing does not alter a company's statutory obligations under Indian law. The following central statutes and state regulations directly govern payroll processing for white-collar employees at large-scale and mid-scale Indian organizations.

| Statute | Applicability | Key Compliance Requirement | Potential Consequences of Non-Compliance | Regulatory Authority |

|---|---|---|---|---|

| Employees Provident Funds and Miscellaneous Provisions Act, 1952 (EPF) | Establishments employing 20 or more employees | Timely EPF registration, monthly ECR filing and contribution remittance | Interest, damages, penalties and legal action for delayed or non-payment | EPFO |

| Employees State Insurance Act, 1948 (ESI) | Applicable establishments with eligible employees as prescribed by law | Timely contribution payment, employee registration and statutory reporting | Monetary penalties and legal proceedings for non-compliance | ESIC |

| Income Tax Act, 1961 (TDS on Salaries) | All employers deducting tax from employee salaries | Accurate TDS deduction, timely deposit, quarterly returns and Form 16 issuance | Interest, penalties and prosecution in severe cases | Income Tax Act, 1961 (TDS on Salaries) |

| Payment of Wages Act, 1936 | Applicable employees as prescribed under the Act | Timely salary disbursement and compliance with authorized deduction rules | Penalties and employee claims for delayed or improper wage payments | Ministry of Labour & Employment |

| Payment of Bonus Act, 1965 | Eligible establishments and employees under the Act | Accurate bonus calculation and timely payment within statutory timelines | Fines and legal action for non-compliance | Ministry of Labour & Employment |

| Professional Tax (State-Specific) | Applicable in notified states | Employee deduction, payment and filing of state-specific returns | State-specific penalties, interest, and notices | State Professional Tax Departments |

| Labour Welfare Fund (State-Specific) | Applicable in participating states | Timely employee and employer contributions and statutory filings | State-specific penalties and compliance actions | State Labour Welfare Boards |

| Payment of Gratuity Act, 1972 | Establishments employing 10 or more employees | Accurate gratuity calculation and timely settlement of eligible employee claims | Interest, penalties, and legal consequences for delayed payment | Ministry of Labour & Employment |

| Digital Personal Data Protection Act, 2023 (DPDP) | Organizations processing personal employee data | Secure handling of payroll data, privacy safeguards, and appropriate data processing controls | Regulatory action and financial penalties for data protection violations | Ministry of Electronics and Information Technology (MeitY) |

Why the principal employer remains legally liable even after Outsourcing Payroll

Indian statutory law recognizes only the registered employer as the accountable entity for labor compliance. A payroll outsourcing contract is a private commercial agreement and does not alter the employer's obligations under government statute.

Under Section 7A of the Employees Provident Funds Act 1952, the EPFO can recover dues directly from the employer through attachment of assets - regardless of any outsourcing arrangement. Similarly, under ESI Act Section 45A, the ESIC assesses contributions and penalties against the employer. Ministry of Labour enforcement advisories (2023) explicitly state that outsourcing of payroll functions does not dilute the principal employer's statutory obligations. The outsourcing vendor has no statutory relationship with EPFO, ESIC or Income Tax authorities.

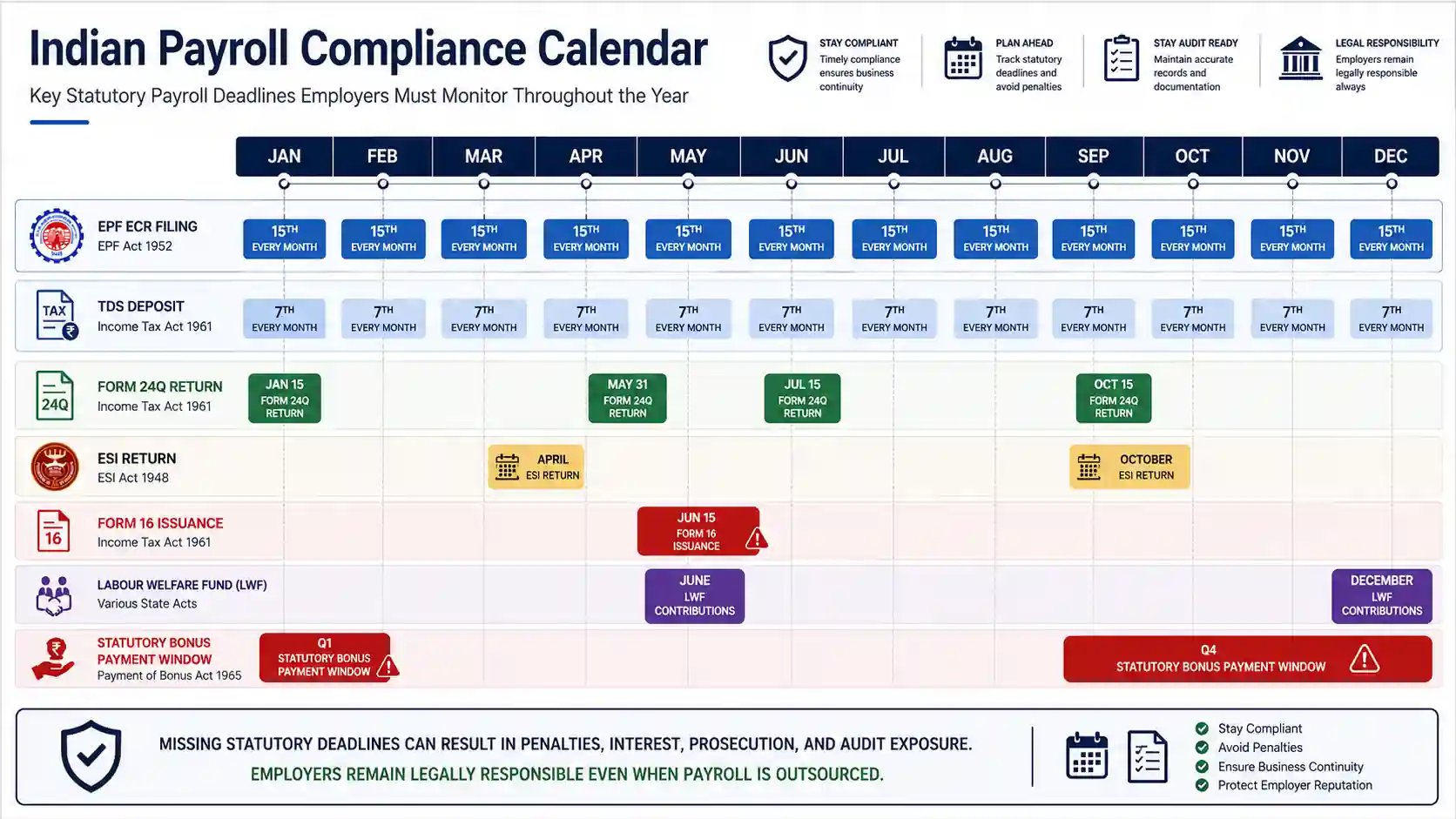

What a Compliant Payroll Vendor must Deliver Every Month: 7 Essential Compliance Tasks

When evaluating a payroll outsourcing vendor for your Indian operations - whether you are a manufacturing company like those served by L&T, an automotive components firm like Aptiv or an engineering enterprise like Andritz - the monthly compliance execution calendar is the most objective performance benchmark. The following framework defines what competent vendors must execute for white-collar workforce payroll every calendar month.

1. Gross-to-Net Salary Computation with Statutory Deductions

Accurate CTC-to-in-hand calculations including Basic Pay, HRA (House Rent Allowance), Special Allowances, LTA, Reimbursements, and variable pay. The vendor must apply current state-wise minimum wages - state governments revise these twice annually (April and October) and apply correct Professional Tax slabs per each employee's work state.

2. EPF Electronic Challan cum Return (ECR) Filing

Monthly ECR submission on the EPFO Unified Employer Portal (unifiedportal-emp.epfindia.gov.in) no later than the 15th of each month. Employer contribution: 12% of Basic + DA - split as 3.67% EPF + 8.33% EPS. Administrative charges: 0.5% EDLI + 0.5% EPF admin. Employee contribution: 12% to EPF. New hire UAN (Universal Account Number) activation and KYC seeding within 30 days of joining. Source: EPFO Circular 2024, Para 38 EPF Scheme 1952.

3. ESI Contribution Deposit and Employee Registration

Monthly deposit of ESI contributions - employee 0.75% + employer 3.25% of gross wages - by the 15th. New employee ESI IP (Insurance Policy) number must be allotted within 10 days of joining; delay creates employer liability for medical claims during the unregistered period. Bi-annual ESI returns must be filed in April and October. Source: ESI Act 1948, Sections 39 and 40.

4. TDS Deduction, Deposit and Quarterly 24Q Return

Monthly TDS deduction from salary based on projected annual income and declared investments under Form 12BB (Section 80C, 80D, HRA, etc.). TDS deposit by the 7th of each month. Quarterly Form 24Q filing: Q1 (July 15), Q2 (October 15), Q3 (January 15), Q4 (May 31). Form 16 issuance to all employees by June 15 annually. Source: Income Tax Act 1961, Section 192; Income Tax India portal.

5. Professional Tax (PT) Compliance - State-wise

State-specific PT slabs must be correctly applied per employee's state of employment. Key rates (May 2025): Maharashtra - ₹200/month for salaries above ₹10,000; Karnataka - ₹200/month above ₹15,000; Tamil Nadu - ₹208/month for most brackets; Andhra Pradesh - ₹150-₹200/month slab-wise. Annual PT enrollment certificate renewal required in each operating state.

6. Labour Welfare Fund (LWF) Contributions - State-wise

State-applicable LWF deductions are typically bi-annual (June and December). Current rates (2025): Karnataka - ₹20 employee + ₹40 employer per year; Maharashtra - ₹6 employee + ₹12 employer per half-year; Tamil Nadu - ₹10 employee + ₹20 employer per half-year; Gujarat - ₹6 employee + ₹12 employer per half-year. Source: Respective State LWF Acts - verified via state labor department portals.

7. Full and Final Settlement (FFS) Processing on Employee Exit

The vendor must accurately compute: gratuity (formula: Last Drawn Basic + DA × 15/26 × Completed Years of Service, under Payment of Gratuity Act 1972); earned leave encashment; notice pay; statutory bonus (pro-rated if applicable); and arrear salary. FFS must be processed within 45 days of separation as per industry best practice. EPF Form 10C/10D and ESI claim support must be provided to the separated employee.

How to Conduct a Quarterly Audit of your Payroll Vendor's Compliance Performance

A structured quarterly audit protocol is the only reliable safeguard against vendor-caused compliance failures. The following checklist covers minimum audit actions for large-scale and mid-scale Indian companies with outsourced payroll.

Quarterly Payroll Vendor Audit Checklist

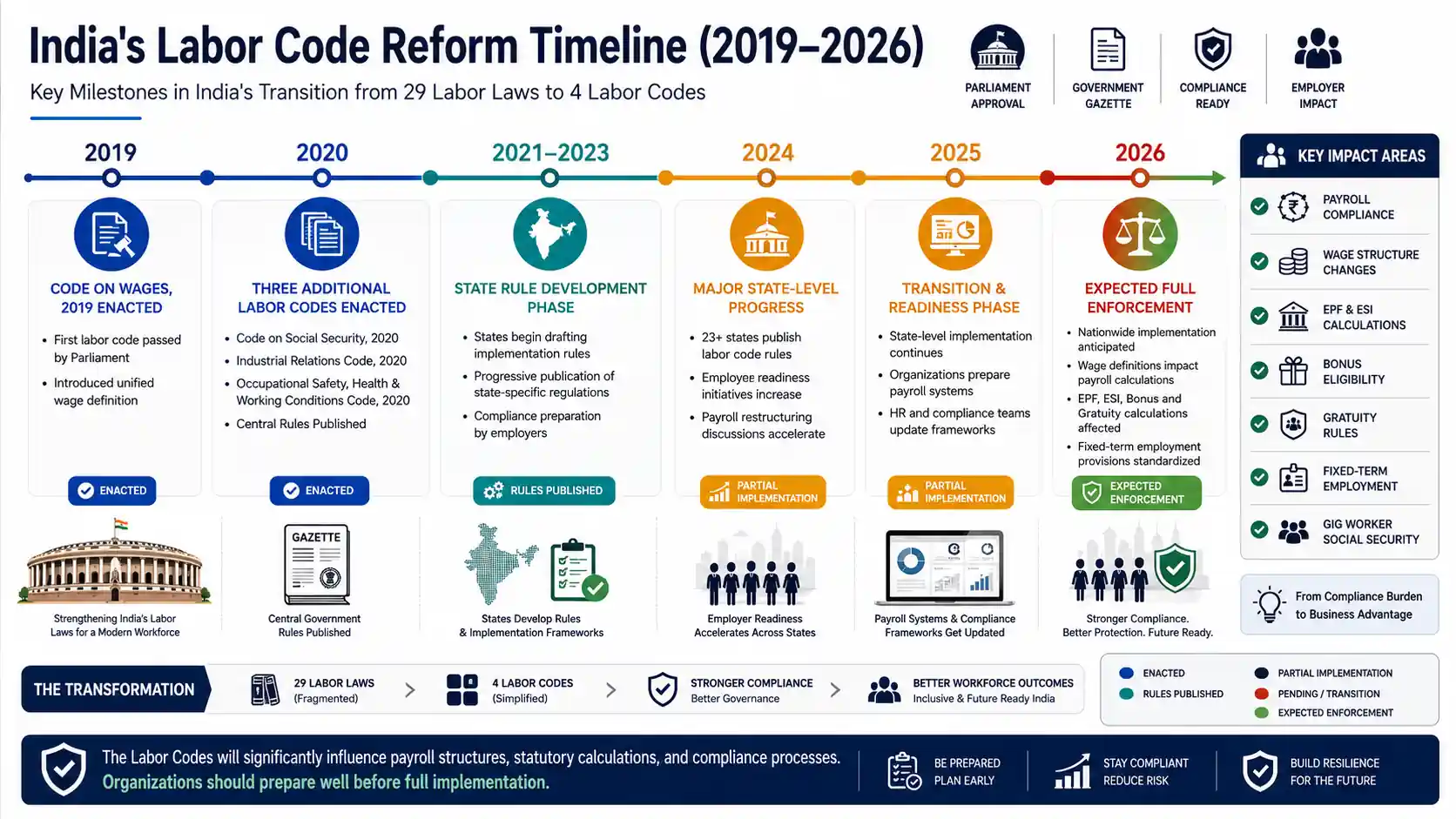

How India's Labor Codes may impact Payroll Compliance

What to include in Your Payroll Outsourcing Contract to Protect Compliance

A payroll outsourcing contract that lacks even one of these provisions leaves your company legally exposed - EPFO adjudication officers have cited the absence of audit rights and indemnification clauses as evidence of employer negligence in Section 7A recovery proceedings, resulting in full penalty liability with no contractual recourse against the vendor.

A. Statutory Filing SLAs with Buffer Dates - Not Just Legal Deadlines

Require the vendor to commit to internal processing cutoffs with a 3-day buffer before statutory deadlines: EPF ECR by the 12th (not 15th); TDS deposit by the 6th (not 7th); ESI by the 12th. A vendor who processes on the deadline date leaves no margin for bank processing delays or system failures. SLA breach should trigger automatic penalty absorption (see clause B).

B. Vendor Penalty Absorption for Vendor-Caused Non-Compliance

The contract must explicitly state that the vendor absorbs all government-levied interest, penalties, and late fees directly caused by vendor processing errors or delays. This clause does not transfer statutory liability (which remains with the employer) but creates a private contractual remedy. Require the vendor to have professional indemnity insurance - verify the policy certificate at signing.

C. Audit Rights - Portal Access and Record Production

Your company must retain the right to: conduct quarterly compliance audits of vendor-maintained records; access all statutory portals (EPFO, ESIC) using company credentials (not shared vendor credentials); receive complete statutory filing reports within 5 business days of any government portal filing. This audit right must survive contract termination for 5 years - the statutory record retention period under most Indian labor laws.

D. Data Processing Agreement (DPA) Under DPDP Act 2023

Payroll data includes Aadhaar numbers, PAN cards, bank account details, salary structures and health information - all classified as personal data under India's Digital Personal Data Protection Act 2023. The vendor is a "Data Processor"; your company is the "Data Fiduciary." A signed DPA defining data use restrictions, breach notification timelines (72 hours) and data deletion protocols is legally mandatory. Source: DPDP Act 2023, Sections 8 and 9; MEITY rules (under finalization as of May 2025).

E. Multi-State Coverage Attestation and Registration Certificates

Require the vendor to provide copies of Professional Tax registration certificates, LWF board registrations, and Shops & Establishments Act registrations for every state in which you have employees. A vendor claiming multi-state capability without documented state registrations is operating outside the compliance framework. Update this list annually and whenever you expand to a new state.

India's 4 Labor Codes: Key Payroll Compliance Changes for Employers

India has consolidated 29 central labor statutes into 4 Labor Codes, enacted between 2019 and 2020. These codes change how wages are defined, how EPF and ESI applicability is calculated and how fixed-term employment is structured for payroll. The following table maps each code's payroll impact and implementation status as of May 2025.

| Labor Code | Key Payroll Impact | Implementation Status - May 2025 |

|---|---|---|

| Code on Wages, 2019 | Redefines "wage" - floor wage applies nationally. Basic salary must constitute at least 50% of CTC; allowances and reimbursements capped at 50%. EPF and ESI calculations will be revised upward for companies that currently keep basic low. | Central rules published (2020). State rules published in 23 states. Full enforcement pending uniform state notification. Source: labour.gov.in, 2024. |

| Code on Social Security, 2020 | Expands EPF/ESI coverage to gig and platform workers. New definition of "employee" broadens applicability. Fixed-term contract employees entitled to gratuity proportionate to service - even for periods less than 5 years. | Central rules published (2020). State rules pending in most states. Implementation timeline: 2025-2026 expected. Source: labour.gov.in. |

| Industrial Relations Code, 2020 | Formalizes fixed-term employment. Payroll must handle statutory benefits proportionally for fixed-term employees. Notice period and retrenchment compensation calculations change for specified establishments. | Central rules published. State implementation partial. Source: labour.gov.in. |

| Occupational Safety, Health & Working Conditions Code, 2020 | Changes working hour definitions and overtime calculation thresholds - directly impacts payroll computation for factory and contract workforce. Overtime rate remains 2x regular wage. | Central rules published. Implementation pending most states. Source: labour.gov.in. |

Common Payroll Compliance Failures When Companies Outsource Payroll

The following compliance failures represent documented patterns in EPFO, ESIC, and Income Tax enforcement actions against Indian companies that had outsourced payroll. Each failure type, its regulatory consequence and its preventable root cause are stated explicitly for direct employer action.

| Late EPF deposit caused by vendor processing delays. | EPFO levies 12% annual interest under Para 38 of EPF Scheme 1952, plus damages of ₹5,000 minimum under Section 14B. Root cause: vendor payroll processing cycle scheduled too close to the 15th deposit deadline. Prevention: require vendor to complete ECR filing by the 12th, building a 3-day operational buffer |

| Incorrect EPF wage base - allowances structured to suppress EPF contributions. | EPFO audit teams now cross-reference Form 26AS salary data against ECR wage figures. Supreme Court ruling in Regional Provident Fund Commissioner v. Vivekananda Vidyamandir (2019) confirmed that allowances paid uniformly to all employees must be included in EPF wages. Prevention: audit EPF wage definition annually against the ruling. |

| New hire ESI registration delayed beyond 10 days. | If a new employee makes a medical claim before their ESI IP number is allotted, the employer bears the full cost of treatment plus penalties under ESI Act Section 85. Root cause: vendors batch-processing new hire registrations monthly rather than weekly. Prevention: contractual SLA requiring ESI registration within 7 days of joining. |

| TDS mismatch for mid-year variable pay and bonuses. | Joining bonuses, performance incentives paid mid-year and ESOP vesting events cause TDS projection errors. This generates Form 26AS mismatches, triggering Section 143(1) income tax notices to employees - damaging trust in the employer's payroll function. Prevention: vendor must re-project TDS every month, not annually. |

| Professional Tax non-compliance when expanding operations to new states. | Companies opening offices in Bengaluru, Hyderabad or Pune after initial payroll setup in Maharashtra frequently miss Karnataka, Telangana or Maharashtra PT registration for new employees. Prevention: vendor must proactively initiate PT registration in any new state within the first hire's first month. |

| Gratuity liability not provisioned in financial statements. | Payroll vendors execute current payroll but do not always maintain the data needed for annual actuarial gratuity valuation. For companies above the AS 15 threshold, an unprovisioned gratuity liability results in qualified audit opinions. Prevention: require vendor to provide employee-wise service data and salary history annually in actuary-ready format. |

10 Most-Asked Questions on Indian Payroll Compliance when outsourcing

The following questions are sourced from actual search behavior of HR managers, business owners, and compliance officers at large-scale and mid-scale Indian companies considering or currently using payroll outsourcing services.

1. If my payroll vendor misses the EPF deposit deadline, who gets penalized - my company or the vendor?

Your company gets penalized. The EPFO issues enforcement notices, interest demands and damage orders exclusively to the registered employer under EPF Act Sections 14B and 7Q. The vendor has no direct statutory relationship with EPFO. Your commercial outsourcing contract may allow you to recover penalties from the vendor via indemnification clauses - but you must first pay the government and then pursue the vendor separately through the contract's dispute resolution process. Penalty: 12% annual interest plus ₹5,000-₹25,000 minimum damages per default period. Source: EPFO enforcement guidelines, epfo.gov.in.

2. What is the minimum EPF and ESI compliance a payroll vendor must handle for a company with 100+ employees?

For a 100-employee company in India, the vendor must: (1) file monthly EPF ECR by the 15th; (2) deposit employer 12% and employee 12% EPF contributions including 0.5% EDLI and 0.5% admin charges; (3) deposit ESI employer 3.25% and employee 0.75% contributions by the 15th; (4) file bi-annual ESI returns in April and October; (5) manage UAN activation and KYC seeding for all new employees within 30 days; (6) allot ESI IP numbers within 10 days of each new hire; (7) process Form 10C and 10D claims for exiting employees. These are non-negotiable minimum obligations under EPF Act 1952 and ESI Act 1948. Source: epfo.gov.in; esic.gov.in.

3. How do I verify that my payroll vendor is actually filing EPF and ESI on time?

Log into the EPFO Unified Employer Portal (unifiedportal-emp.epfindia.gov.in) using your establishment credentials - not the vendor's login. Under the Payments section, verify the ECR challan submission date for each month. For ESI, log into the ESIC employer portal (esic.gov.in) under your company's credentials and review the contribution deposit history. Do not rely on vendor-generated compliance reports alone - always cross-verify directly against government portals. Perform this check monthly, not quarterly, so you detect issues within the same filing cycle.

4. Does outsourcing payroll protect my company from Indian labor law audits and inspections?

No. Outsourcing payroll does not protect a company from labor law audits or inspections. EPFO, ESIC, and state labor inspectors visit company premises and demand records from the employer - the existence of a payroll outsourcing arrangement is not a legally recognized defense under EPF Act Section 7A or ESI Act Section 45A. The genuine protection that payroll outsourcing provides is operational: a competent vendor ensures your records are accurate and audit-ready, your statutory filings are on time, and your documentation is complete - so that when an audit happens, you have nothing to conceal. Source: EPF Act 1952 Sections 7A and 14B; ESI Act 1948 Section 85.

5. What is the current EPF contribution rate for employers in India in 2025?

As of May 2025, the employer EPF contribution rate is 12% of an employee's Basic Salary plus Dearness Allowance. This 12% is split as: 3.67% credited to the individual EPF account and 8.33% credited to the Employees' Pension Scheme (EPS). Additionally, employers pay 0.5% EDLI (Employees' Deposit Linked Insurance) contribution and 0.5% EPF administrative charges. Employee contribution is 12%, entirely credited to the EPF account. Both employer and employee contributions are computed on the actual Basic + DA or on a ceiling of ₹15,000 per month for EPS computation purposes. These rates have been unchanged since 2020.

6. Can a mid-size company with 200 employees in multiple states use a single payroll outsourcing vendor?

Yes and multi-state payroll management is precisely where professional payroll outsourcing delivers the greatest compliance value. A competent vendor manages state-specific Professional Tax slabs, Labour Welfare Fund contribution rates, Shops & Establishments Act compliance, and minimum wage revisions for every state where you have employees. Before signing, require the vendor to provide a state-wise compliance coverage matrix listing their active PT, LWF and S&E registrations in each state where you operate. A vendor without documented state registrations in your operating states is not multi-state capable in practice.

7. What happens to EPF and ESI records when we switch payroll vendors?

EPF and ESI records are owned by the government and by your company - not by the vendor. The Universal Account Number (UAN) is linked to the individual employee and persists across all employer and vendor changes. When switching vendors: (1) ensure the new vendor obtains your EPFO employer establishment login credentials - these are company-owned, not vendor-owned; (2) transfer complete payroll data files in a structured, mutually agreed format (including YTD earnings, TDS workings, and PT history); (3) verify the new vendor completes the first EPF ECR filing without a gap month; (4) update the authorized signatory on the ESIC portal before the first ESI return under the new vendor. ESI registration remains with your company throughout - only portal access transitions.

8. Is sharing employee payroll data with an outsourcing vendor covered under India's DPDP Act 2023?

Yes. When you share employee payroll data - including Aadhaar, PAN, bank account details, salary structures and health-related information for ESI — with a payroll vendor, that vendor becomes a "Data Processor" under India's Digital Personal Data Protection Act 2023 (DPDP Act). Your company is the "Data Fiduciary." Legal obligations: (1) execute a signed Data Processing Agreement (DPA) before data sharing begins; (2) ensure employees have provided valid consent for payroll data processing, documented during HR onboarding; (3) confirm the vendor has data breach notification protocols meeting the 72-hour CERT-In standard. DPDP penalty for data breach: up to ₹250 crore per incident. Source: DPDP Act 2023, Sections 8 and 9; MEITY (meity.gov.in), Rules under finalization as of May 2025.

9. How often should large companies formally audit their payroll vendor's compliance performance?

Large-scale companies with 500+ employees should follow a three-tier audit schedule: (1) Monthly - direct portal verification of EPF ECR and ESI challan submission dates via government portals, not vendor reports. (2) Quarterly - formal compliance audit covering all statutory filings for the quarter, payslip accuracy sampling (minimum 5% of headcount), new hire and exit processing compliance review and state-specific minimum wage application verification. (3) Annual - full reconciliation of Form 26AS against 24Q returns, EPF passbook verification for all employees, ESI contribution history audit, actuarial data for gratuity provisioning and DPDP compliance review of the Data Processing Agreement.

Why Choose Voltech HR Services for Payroll Outsourcing

Managing payroll compliance across Indian labor laws requires more than payroll processing software. It requires a partner with the expertise, processes and compliance focus needed to support your workforce across multiple locations and regulatory frameworks.

Payroll Compliance is a Business Risk, Not Just an HR Function

Payroll outsourcing can improve efficiency, reduce administrative burden and provide access to specialized compliance expertise. However, Indian labor laws place statutory responsibility squarely on the employer, regardless of who processes payroll. EPF, ESI, TDS, Professional Tax, Labour Welfare Fund, gratuity and data privacy obligations remain the employer's legal responsibility and cannot be outsourced.

The organizations that achieve long-term payroll compliance are those that treat payroll as a governance function rather than a transactional process. They select vendors based on compliance capability, maintain visibility into statutory filings, conduct periodic audits and build accountability into every payroll workflow.

As labor regulations evolve, state-level compliance requirements continue to expand, and the implementation of India's Labor Codes approaches, businesses must ensure their payroll operations remain accurate, transparent and audit-ready. A proactive compliance framework not only reduces regulatory risk but also strengthens employee trust, financial control and operational stability.

Ultimately, successful payroll outsourcing is not defined by whether salaries are processed on time. It is defined by whether an organization can confidently demonstrate compliance, withstand regulatory scrutiny and adapt to changing labor laws without disruption to its workforce or business operations.

Related Resources for Employers & HR Leaders

Looking to improve workforce planning, compliance readiness and payroll operations? Explore these practical guides:

→ Contract Staffing in India: The 2026 Workforce Strategy Guide - Learn how contract staffing is helping Indian businesses address labour shortages, manage fluctuating workforce demand, and improve operational flexibility. Explore workforce planning strategies, compliance considerations, cost control measures and best practices for building scalable staffing models across manufacturing, logistics, infrastructure and industrial sectors.

→ Labour Inspector Visit Checklist for Indian Employers (2026 Edition) - Prepare your organization for labour inspections with a comprehensive compliance checklist covering employee records, statutory registers, wage documentation, EPF, ESI, contractor compliance, working hours, safety records and labour law documentation. Understand what inspectors typically review and how to reduce compliance risks during inspections.

→ Why Delaying Your 2026 Payroll Switch Could Cost You ₹29 Lakhs - Understand the hidden financial and compliance risks of postponing payroll modernization under India's evolving labour regulations. Learn how outdated payroll structures can create wage definition issues, EPF and gratuity liabilities, compliance penalties, and operational inefficiencies and how proactive payroll planning helps organizations stay compliant and financially protected.

Ready to Simplify Your Staffing and Payroll Operations?

Contact our team for a free consultation on staffing, payroll management and statutory compliance solutions tailored to your workforce requirements.

www.voltechhrservices.comOverseas & Domestic Recruitment | Staffing & Payroll | Background Verification | Corporate Events

Write Comment